TIMELINE OF USURY INTEREST FRAUD!

USURY = The practice of lending money and charging the borrower exorbitant interest.

Bible called USURY INTEREST an “abominable thing,” in line with rape, murder, robbery & idolatry.

Jewish Talmud forbids Jews ripping each other off with USURY, but says it is a great thing to do to a NON-JEW.

A timeline of Consumer Credit – Americans now have over $12.4 Trillion borrowed through mortgages, credit cards, student loans, auto loans, and other types of credit.

What do Hammurabi, Plato, Charlemagne, Dante and Queens Mary and Elizabeth have in common? They all condemned, outlawed or regulated the charging of interest on loans.

3,500 BCE: USURY INTEREST – Sumer was the first urban civilization – with about 89% of its population living in cities. It is thought that here consumer loans, used for agricultural purposes, were first used.

1,800 BCE: USURY INTEREST — Babylon – The Code of Hammurabi was written, formalizing the first known laws around credit. Hammurabi established the maximum interest rates that could be used legally: 33.3% per year on loans of grain, and 20% per year on loans of silver. To be valid, loans had to be witnessed by a public official and recorded as a contract. The Code of Hammurabi regulates the interest that can be charged on a loan and most loans were made below the legal limit.

800 BCE-600 BCE: USURY INTEREST — Both Plato and Aristotle believed usury was immoral and unjust. The Greeks at first regulate interest, and then deregulate it. After deregulation, there was so much unregulated debt that Athenians were sold into slavery and threatened revolt.

443 BCE: USURY INTEREST — The Romans adopt the “Twelve Tables” and cap interest at 8 1/3%.

88 BCE: USURY INTEREST — The Roman usury rate is raised to 12%.

50 BCE: USURY INTEREST — The Roman Republic Around this time, Cicero noted that his neighbor bought 625 acres of land for 11.5 million sesterces. Did this person literally carry 11.5 tons of coins through the streets of Rome? No, it was done through credit and paper. Cicero writes “nomina facit, negotium conficit” – or, “he uses credit to complete the purchase”.

533 AD: USURY INTEREST – The Roman “Code of Justinian” sets a graduated maximum interest rate at 8.33% for loans to ordinary citizens. This law lasted 1010 years until 1543 AD

600s AD: USURY INTEREST – The Quran states: “…those you take usury will arise on the Day of Resurrection like someone tormented by Satan’s touch. That is because they say ‘Trade and usury are the same,’ But God has allowed trade and forbidden usury. Whoever, on receiving God’s warning, stops taking usury make keep his past gains — God will be his judge — but whoever goes back to usury will be an inhabitant of the Fire, therein to remain.”

800 AD: USURY INTEREST – Charlemagne outlaws interest throughout his empire. The Dark Ages in Europe. After the collapse of the Western Roman Empire, economic activity ground to a halt. The Church even banned usury, the practice of charging interest on loans, for all laymen under Charlemagne’s rule (768-814 AD). Medieval Canon Law Usury is punishable by ex-communication. Medieval Roman Law Usurer’s are fined 4X the amount taken, while robbery is penalized at twice the amount taken.

1000 AD: USURY INTEREST – In England, the charging of any interest is punishable by taking the usurer’s land and chattels.

1306 AD-1321 AD: USURY INTEREST – Dante pens “The Inferno,” in which he places usurers at the lowest ledge in the seventh circle of hell – lower than murderers.

1500 AD: USURY INTEREST — The Age of Discovery – As European explorers and merchants begin trade missions to faraway lands, the need for capital and credit increases.

1545 AD: USURY INTEREST — England – After the Reformation, the first country to establish a legal rate of interest was England in 1545 during the reign of Henry VIII. The rate was set at 10%.

1553 AD-1558 AD: USURY INTEREST – During the reign of Queen Mary, English Parliament again disallows the collection of interest.

1570 AD: USURY INTEREST – During the Reign of Queen Elizabeth, interest rates in England are limited to under 10%. This law lasts until 1854.

1700s AD: USURY INTEREST – American colonies adopt usury laws, setting the interest cap at 8%.

1713 AD: USURY INTEREST – Adoption in England of the “Statue of Anne,” an Act to reduce interest rates.

1776 AD-1800s AD: USURY INTEREST – All of the States in the Union adopt a general usury. Most states set the interest limit at 6%.

1787 AD: USURY INTEREST — England – Philosopher Jeremy Bentham writes a treatise called “A Defense of Usury”, arguing that restrictions on interest rates harm the ability to raise capital for innovation. If risky, new ventures cannot be funded, then growth becomes limited.

1803 AD: USURY INTEREST — England The birth of modern consumer credit. Credit reporting itself originated in England in the early 19th century. The earliest available account is that of a group of English tailors that came together to swap information on customers who failed to settle their debts.

1826 AD: USURY INTEREST — England – The Manchester Guardian Society is formed, and later begins issuing a monthly newsletter with information about people who fail to pay their debts.

1841 AD: USURY INTEREST — New York – The Mercantile Agency is founded, and starts systematized rumors about the character and assets held by debtors through a network of correspondents. Massive ledgers in New York City are made, though these reports were heavily subjective and biased.

1864 AD: USURY INTEREST — New York – The Mercantile Agency is renamed the R. G. Dun and Company on the eve of the Civil War, and finalizes an alphanumeric system for tracking creditworthiness of companies that would remain in use until the twentieth century.

1899 AD: USURY INTEREST — Atlanta – The Retail Credit Company was founded, and begins compiling an extensive list of creditworthy customers. Later on, the company would change its name to Equifax. Today, it is the oldest of the three major credit agencies today in the United States.

Pre-1900s AD: USURY INTEREST – Interest rates in United States were CAPED at or near 10%.

1900 AD-1979 AD: USURY INTEREST – Loan laws provided some CAPS on interest rates in every state.

1908 AD: USURY INTEREST — Detroit The consumer credit boom – Henry Ford’s Model T makes automobiles accessible to the “great multitude” of people, but they were still too expensive to buy with cash for most families.

1910s AD: USURY INTEREST – A move to deregulation causes 11 states to eliminate their usury laws. Nine more states raise the usury cap to 10% or 12%. Banks are not making personal loans. “Salary Lenders” fill the need by “purchasing” a worker’s future wages in exchange for a high fee – equal to a lending rate of 10% – 33%.

1916 AD: USURY INTEREST – A Uniform Small Loan Law allows specially licensed lenders to charge higher interest rates—up to 36%—in return for adhering to strict standards of lending.

1919 AD: USURY INTEREST — Detroit – GM solves this problem by loaning consumers the money they need to buy a new car. General Motors Acceptance Corporation (GMAC) is founded and popularizes the idea of installment plan financing. Consumers can now get a new car with just a 35% down payment at time of financing.

1930 AD: USURY INTEREST — United States – By this time, efficient U.S. factories are pumping out cheaper consumer products and appliances. Following the lead of GM, now washing machines, furniture, refrigerators, phonographs, and radios can be bought on installment plans. It’s also worth noting that in this period, 2/3 of all autos are bought on installment plans.

1945-1979 AD: USURY INTEREST – All states adopt special loan laws that cap interest at higher than the general usury rate—at 36%—but cap it nevertheless.

1950 AD: USURY INTEREST — United States The first in big data – Typical middle-class Americans already had revolving credit accounts at different merchants. Maintaining several different cards and monthly payments was inconvenient, and created a new opportunity. At the same time, Diners Club introduces their charge card, which helps open the floodgates for other consumer credit products.

1955 AD: USURY INTEREST — United States – Early credit reporters use millions of index cards, sorted in a massive filing system, to keep track of consumers around the country. To get the latest information, agencies would scour local newspapers for notices of arrests, promotions, marriages, and deaths, attaching this information to individual credit files.

1958 AD: USURY INTEREST — United States – BankAmericard (now Visa) is “dropped” in Fresno, California. American Express and Mastercard soon follow, offering Americans general credit for a wide range of purchases.

1960 AD: USURY INTEREST — United States – At a time when the technology was limited to filing cabinets, the postage meter, and the telephone, American credit bureaus issued 60 million credit reports in a single year.

1964 AD: USURY INTEREST — United States – The Association of Credit Bureaus in the U.S. conducts the first studies into the application of computer technologies to credit reporting. Accuracy of data is also improved around this time by standardizing credit application forms.

1970 AD: USURY INTEREST — United States – The first Fair Credit Reporting Act is passed in the United States. It establishes a standard legal framework for credit reporting agencies.

1978 AD: USURY — Marquette vs. First of Omaha – Supreme Court allows banks to export the usury laws of their home state nationwide and sets off a competitive wave of deregulation, resulting in the complete elimination of usury rate ceilings in South Dakota and Delaware, among others.

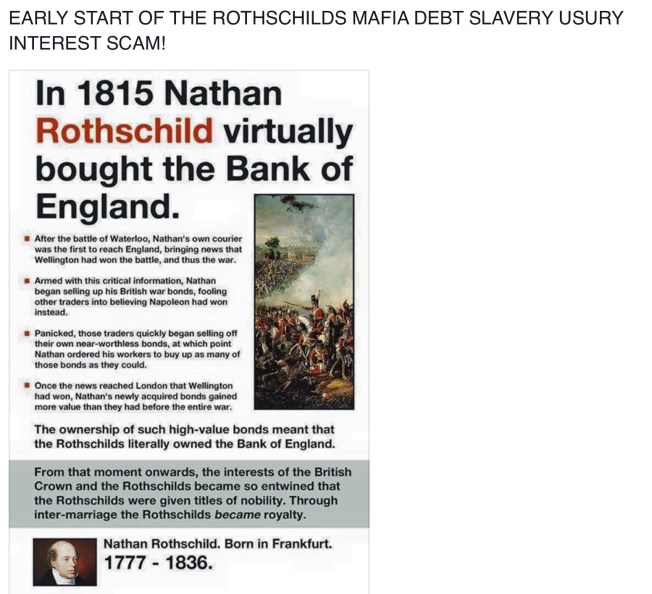

1979 AD: USURY INTEREST – Reagan decided to remove all caps on Interests Rates as British Rothschilds Crime Syndicate told Reagan to put profits before people.

1979 AD-Today: USURY INTEREST – Lending industry has USURY RATES spiraling out of control to 3,500% or more.

1977 AD: USURY INTEREST – The federal government passes the “Community Reinvestment Act” (CRA) which requires banks to invest in their communities.

1978 AD: USURY INTEREST – The US Supreme Court decides that national banks may export the state interest rate law of their home state into any state where they do business. In response, South Dakota eliminates its interest rate caps. Several credit card issuing banks move to South Dakota and operate nationally with no interest rate cap.

1980s AD: USURY INTEREST — United States – The three biggest credit bureaus attain universal coverage across the country.

1980 AD: USURY INTEREST – Congress preempts state interest rate controls on all first lien mortgages. This enables predatory mortgage lenders to make seemingly affordable loans, like adjustable rate and interest-only loans, that lead to foreclosure for many.

1980 AD: USURY — Depository Institutions Deregulation and Monetary Control Act – Legislation

increases deposit insurance from $40,000 to $100,000, authorizes new authority to thrift institutions, and calls for the complete phase-out of interest rate ceilings on deposit accounts.

1982 AD: USURY — Garn-St. Germain Depository Institutions Act – Bill deregulates thrifts almost entirely, allowing commercial lending and providing for a new account to compete with money market mutual funds. This was a Reagan administration initiative that passed with strong bi-partisan support.

1987 AD: USURY — FSLIC Insolvency – GAO declares the deposit insurance fund of the savings and loan industry to be insolvent as a result of mounting institutional failures.

1989 AD: USURY — Financial Institutions Reform and Recovery Act – Act abolishes the Federal Home Loan Bank Board and FSLIC, transferring them to OTS and the FDIC, respectively. The plan also creates the Resolution Trust Corporation to resolve failed thrifts.

1989 AD: USURY INTEREST — United States – The FICO score is introduced, and quickly becomes a standard system to measure credit scores based on objective factors and data.

1994 AD: USURY INTEREST – Congress adopts the Home Ownership and Equity Protection Act of 1994, which provides some substantive protections to home mortgage borrowers with interest rates or points that are extraordinarily expensive, but sets no limits on what can be charged for these loans.

1994-2005 AD: USURY INTEREST – Many states and cities try to protect their citizens by adopting state statutes and local ordinances to curb predatory lending, but preemption claims by the federal government impede their efforts. Numerous bills are introduced in Congress to protect consumers in a wide range of transactions, including rent-to-own, credit cards, payday lending, and predatory mortgage lending, but none of these bills makes it to a hearing.

1994 AD: USURY — Riegle-Neal Interstate Banking and Branching Efficiency Act – This bill eliminated previous restrictions on interstate banking and branching. It passed with broad bipartisan support.

1996 AD: USURY — Fed Reinterprets Glass-Steagall – Federal Reserve reinterprets the Glass-Steagall Act several times, eventually allowing bank holding companies to earn up to 25 percent of their revenues in investment banking.

1998 AD: USURY — Citicorp-Travelers Merger – Citigroup, Inc. merges a commercial bank with an insurance company that owns an investment bank to form the world’s largest financial services company.

1999 AD: USURY — Gramm-Leach-Bliley Act – With support from Fed Chairman Greenspan, Treasury Secretary Rubin and his successor Lawrence Summers, the bill repeals the Glass-Steagall Act completely.

2000 AD: USURY — Commodity Futures Modernization Act – Passed with support from the Clinton Administration, including Treasury Secretary Lawrence Summers, and bi-partisan support in Congress. The bill prevented the Commodity Futures Trading Commission from regulating most over-the-counter derivative contracts, including credit default swaps.

2001 AD–2007 AD: USURY INTEREST – Predatory and mainly subprime lenders make home loans to people who cannot afford them, boosting their own profits in the short-term. Many of these loans are packaged and sold to Wall Street.

2004 AD: USURY — Voluntary Regulation – The SEC proposes a system of voluntary regulation under the Consolidated Supervised Entities program, allowing investment banks to hold less capital in reserve and increase leverage.

2005 AD: USURY INTEREST – After extensive pressure from the industry, the federal government changes bankruptcy laws, making it harder for consumers to discharge debts and get a clean start in bankruptcy.

2006 AD: USURY INTEREST – Congress passes the “Talent Amendment” which caps interest on loans made to active military personnel and their families at 36%, reacting to findings that high-cost payday lenders had been targeting the military.

2006 AD: USURY INTEREST — United States – VantageScore is created through a joint-venture between the top three credit scoring agencies. This new consumer credit-scoring model is used by 10% of the market, and 6 of the 10 largest banks use VantageScore.

2007 AD: USURY — Subprime Mortgage Crisis – Defaults on subprime loans send shockwaves throughout the secondary mortgage market and the entire financial system.

2007 AD: USURY INTEREST – Foreclosure rates begin to increase dramatically as a result of predatory mortgage lending.

2007 AD: USURY — December – Term Auction Facility – Special liquidity facility of the Federal Reserve lends to depository institutions. Unlike lending through the discount window, there is no public disclosure on loans made through this facility.

2008 AD: USURY — March – Bear Stearns Collapse – The investment bank is sold to JP Morgan Chase with assistance from the Federal Reserve.

2008 AD: USURY — March – Primary Dealer Facilities – Special lending facilities open the discount window to investment banks, accepting a broad range of asset-backed securities as collateral.

2008 AD: USURY — July – Housing and Economic Recovery Act – Provides guarantees on new mortgages to subprime borrowers and authorizes a new federal agency, the FHFA, which eventually places Fannie Mae and Freddie Mac into conservatorship.

2008 AD: USURY — September – Lehman Brothers Collapse – Investment bank files for Chapter 11 bankruptcy.

2008 AD: USURY — October – Emergency Economic Stabilization Act – Bill authorizes the Treasury to establish the Troubled Asset Relief Program to purchase distressed mortgage-backed securities and inject capital into the nation’s banking system. Also increases deposit insurance from $100,000 to $250,000.

2008 AD: USURY — Money Market Liquidity Facilities – Federal Reserve facilities created to facilitate the purchase of various money market instruments.

2008 AD: USURY INTEREST – Unpaid mortgages cause mortgage-backed securities on Wall Street to continue to “go bad,” triggering widespread economic downturn in both the United States and around the world. Some commercial and investment banks go bankrupt, and some are the object of government “bailouts.”

2009 AD: USURY INTEREST – The passage of the Credit CARD Act, which greatly curtails abusive credit card lending.

2009 AD: USURY — Public-Private Investment Program – Treasury Secretary Timothy Geithner introduces his plan to subsidize the purchase of toxic assets with government guarantees.

2010 AD: USURY INTEREST – The passage of the Dodd-Frank Wall Street Reform and Consumer Protection Act, which creates a Consumer Financial Protection Bureau to rein in predatory lending (though it cannot pass usury caps). The bill also reforms some of Wall Street’s greedy and excessive practices.

Reblogged this on Rangitikei Enviromental Health Watch.

LikeLike

Thank you for the good writeup. It if truth be told was once a amusement

account it. Look advanced to far introduced agreeable from you!

However, how could we communicate?

LikeLike